The sputtering rise in interest rates here in the U.S. resumed this week as rumours of Fed "taper" resurfaced. Still, interest rates remain far below where they were in 2011 due to the relentless deflationary pressures outweighing Fed intervention. However, the real action this week was in Europe, where policy-makers have boxed themeselves in, between weak economic growth and bankruptcy i.e. slow pain or fast pain. All roads lead to collapse...

No Exit Strategy

The European Central Bank surprised world financial markets on Thursday when it lowered interest rates by a quarter of a percentage point. At the same time, the U.S. jobs report also surprised markets with its (relative) strength. Taken together, these two data points told markets to expect ECB easing and Fed tightening. Unfortunately the entire stock market rally of the past two years was predicated on just the exact opposite.

No Grecovery

The other piece of the puzzle came via ZH who indicated that deflation in the Euro Zone periphery (aka. Greece, Spain etc.) was the worst in 50 years. The ECB tight money policy over the past two years strengthened the Euro to bolster the carry trades and finance the periphery debt, but in the meantime it continued to tank the underlying economies as exports were no longer competitive. It was all just a short-term, short-sighed strategy meant to placate financial markets at the expense of the broader economy and average citizen.

This is Where it Gets "Interesting"

The footprint of the carry trades can bee seen in the charts below. The U.S. easing policy aka. QE "Infinity" weakened the dollar, strengthened the Euro and sent dollars overseas to Greece, Spain etc. to buy their bonds and suppress their interest rates:

Spain 10 Year Yield (interest rate) Peaked in July 2012

QE "Infinity" Commenced In September of 2012

http://www.bloomberg.com/quote/GSPG10YR:IND

http://www.bloomberg.com/quote/GSPG10YR:IND

The Euro Bottomed out At the Same Time ~July 2012

The Euro has been strengthening for ~15 months, but is now starting to weaken again, sensing an impending "change" in monetary conditions:

Spanish stocks (red) with Euro (blue)

Spanish stock market strength, which was full "Twilight Zone" this year, was purely a function of Euro strength and the carry trades, now coming off the boil...

Extend and Pretend to the Very End

European policy-makers in collusion with the Fed, bought Wall Street a couple of years with the above contrivance, at the expense of the local European economies. This debt "financing" strategy was never going to work long term, so its efficacy can be expressed merely in terms of re-election cycles. At least one well publicized European re-election occurred in this interim timeframe. Now however, the underlying monetary forces are going in reverse as we see above. Not to say that the Greek and Spanish economies will come roaring back to life, but the financing support - weak dollar, strong Euro for the carry trades is already starting to reverse quite quickly. Unfortunately, this model does not work in reverse, so it will all unwind rather abruptly as over-leveraged speculators all try to get out the same door at the same time.

A Jedi Mind Trick for Weak Minded Investors and Other Fools

Global Central Banks have done nothing to resolve the underlying economic solvency issues. All they have done is buy politicians more time to do nothing while economic solvency only worsened in the meantime. Any investor who is bullish at this juncture is willfully ignoring the fact that nothing has improved since the last financial crisis other than to shift the ongoing debt accumulation burden from private to public; so there is absolutely no reason to believe that it can't happen again at a moment's notice. The widespread delusional assumption of this era is that the 2008 financial crisis was a "generational event". That assumption is going to cause generational bankruptcy.

A Jedi Mind Trick for Weak Minded Investors and Other Fools

Global Central Banks have done nothing to resolve the underlying economic solvency issues. All they have done is buy politicians more time to do nothing while economic solvency only worsened in the meantime. Any investor who is bullish at this juncture is willfully ignoring the fact that nothing has improved since the last financial crisis other than to shift the ongoing debt accumulation burden from private to public; so there is absolutely no reason to believe that it can't happen again at a moment's notice. The widespread delusional assumption of this era is that the 2008 financial crisis was a "generational event". That assumption is going to cause generational bankruptcy.

Sudden Death Borrowed Overtime

Bank for International Settlements: 83rd Annual Report [April 2013]

Page 5:

"Central bank accommodation has borrowed time...but the time has not been well used"

"Low interest rates have made it easy to postpone deleveraging and ...easy for governments to finance deficits and easy to delay reforms in the real economy and financial system"

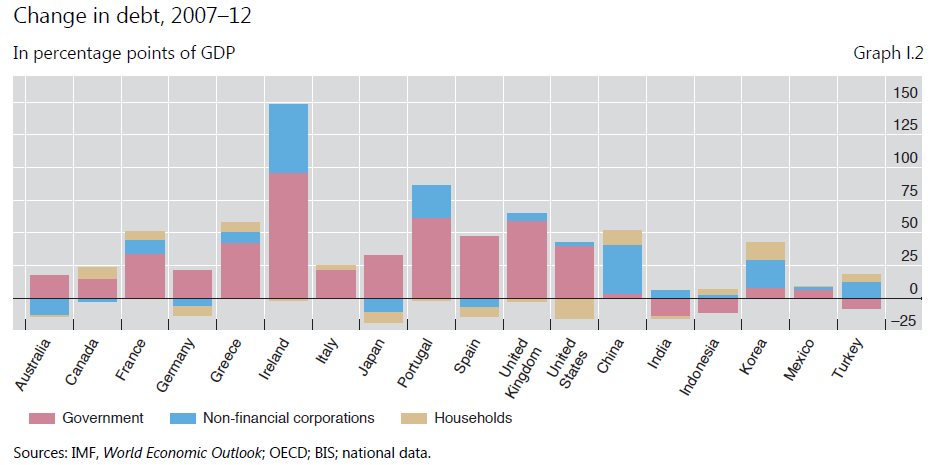

"In the half decade since the financial crisis, the hope was that significant progress would be made in the deleveraging process, thereby enabling a self-sustaining recovery...instead total debt as a share of GDP grew from 2007 to 2012 by $33 trillion":

"Clearly this is unsustainable"...

Page 11:

"Delivering further monetary stimulus is becoming increasingly perilous"

"Six years have passed since the eruption of the global financial crisis, yet robust, self-sustaining, well-balanced growth still eludes the global economy"

So, in a nutshell, the Idiocracy has opted to "solve" a debt crisis by borrowing more money. Anyone who is optimistic as to how this all turns out, is free basing Prozac...

Page 5:

"Central bank accommodation has borrowed time...but the time has not been well used"

"Low interest rates have made it easy to postpone deleveraging and ...easy for governments to finance deficits and easy to delay reforms in the real economy and financial system"

"In the half decade since the financial crisis, the hope was that significant progress would be made in the deleveraging process, thereby enabling a self-sustaining recovery...instead total debt as a share of GDP grew from 2007 to 2012 by $33 trillion":

"Clearly this is unsustainable"...

Page 11:

"Delivering further monetary stimulus is becoming increasingly perilous"

"Six years have passed since the eruption of the global financial crisis, yet robust, self-sustaining, well-balanced growth still eludes the global economy"

So, in a nutshell, the Idiocracy has opted to "solve" a debt crisis by borrowing more money. Anyone who is optimistic as to how this all turns out, is free basing Prozac...